It recently announced relatively positive half-year results, so I thought this would be a good time to review the company’s current situation, its underlying qualities and to estimate fair value and good value prices for its shares.

Table of Contents

- Next’s headline interim results were good

- Next’s strategic priority is to maximise the benefits of being a hybrid online/offline retailer

- The outlook for 2022 and beyond looks positive

- Why Next is in the UK Dividend Stocks model portfolio

- Next has produced consistently high returns and growth

- Next has several durable competitive advantages

- Estimating Next's future dividends

- Estimating fair value, good value and the margin of safety

Next’s headline interim results were good

- Website: nextplc.co.uk

- Results: FY 2022 interim results

Next performed well through the first half of 2021. Both revenues and earnings were ahead of pre-pandemic levels and in June and July, full-priced sales were an impressive 20% up on 2019. A sizeable special dividend has been paid and ordinary dividends are expected to return next year.

This is all good news but much of this rebound has been driven by one-off factors, including:

-

huge amounts of support provided by the government for large parts of the UK economy;

-

record savings rates as people battened down the hatches, leaving them with lots of spending firepower for when the economy reopened;

-

pent-up demand which was released once the lockdown was over, and

-

reduced spending on international holidays, leaving shoppers with more money to spend on clothing.

In addition to these one-off factors, Next has come through the pandemic in reasonably good shape at least partly due to three lucky breaks:

-

Lucky break 1: About two-thirds of its stores are retail park superstores rather than smaller high street stores. In general, retail parks performed much better during the pandemic than high streets, as they’re larger and more open which makes it easier to avoid crowds and social distancing.

-

Lucky break 2: Before the pandemic, about 60% of Next’s sales came from products that either benefitted from lockdowns or were only mildly impacted. These include homewares (where sales took off like a rocket), childrenswear, sportswear, loungewear and underwear.

-

Lucky break 3: Online sales had overtaken store sales even before the pandemic. For obvious reasons, having large-scale and mature online operations was exactly what Next needed given that all non-essential retail stores would be closed for quite some time.

It's clear that much of Next’s success at navigating a path through the pandemic was down to luck, but even so, I think the company has put in a very credible performance.

Of course, Next’s path through the pandemic has been very lopsided and its retail stores recorded a loss during the first half. But the situation is rapidly returning to normal, albeit a new normal with yet more shopping done online.

Looking beyond the headline results, Next has continued to evolve with the times and in 2020, more than half its sales were generated online.

That's a good start, but the company still has a large estate of stores and, thanks to the internet and smartphones, that side of the business has been declining for years.

For example, over the last 17 years, Next’s store-based sales have declined by 39% and in inflation-adjusted terms, that’s going to be more like 60%. This decline is expected to continue with no obvious end in sight.

But it isn’t all doom and gloom and so far at least, those lost in-store sales have mostly migrated to online sales, which have increased by more than 400% over the last 17 years.

In addition, Next can offer customers many more choices online than in a physical store, so in recent years it has vastly expanded its product range. This is good because a wider range of products means there are more reasons for customers to visit Next's website and more items for them to buy when they get there.

Also, Next now also offers thousands of third-party products through its LABEL business, including unique licenced products such as (Ted) Baker childrenswear. This has helped its online sales to more than offset the decline of in-store sales, leading to overall revenue growth in the last decade despite the disruptive impact of the mobile internet.

Given the success of Next's third-party LABEL business, which gives third-party brands access to its website and delivery/returns service, the company has decided to take the idea a step further. Its new service, Total Platform, gives third-party brands an own-branded website running on Next’s e-commerce platform in addition to warehousing, delivery and returns services.

Total Platform is expected to generate revenues of around £200 million in 2021, compared to revenues of around £4 billion for the whole company. So it’s early days, but this is certainly an interesting way to increase the return from all the investment Next has put into its online business.

In Spring 2022, Next is hoping to launch on its Total Platform. This will be by far the largest client for Total Platform, so it’s an important milestone and should be followed in the summer by .

Looking slightly longer-term, management expects online growth to be constrained until a new automated warehouse is up and running in 2023. Even with that constraint, management is optimistic that Next can return to consistent long-term growth, driven by an ever-increasing range of Next and third-party products sold through the Next and Total Platform websites.

And of course, there are lots of concerns at the moment around inflation, labour shortages, supply chain disruption, rising taxes and so on.

These are all potential headwinds, but in all honesty, nobody knows exactly how these things will pan out. So rather than worrying too much about economic uncertainty, I prefer to stick with robust high-quality companies on the assumption that whatever the economy throws at them, their long-term performance is likely to be above average.

So Next has continued to progress well, which is nice because it's been in the UK Dividend Stocks model portfolio since 2016 (back when it was known as the UK Value Investor portfolio), so obviously I think Next is a high-quality business.

Here's why.

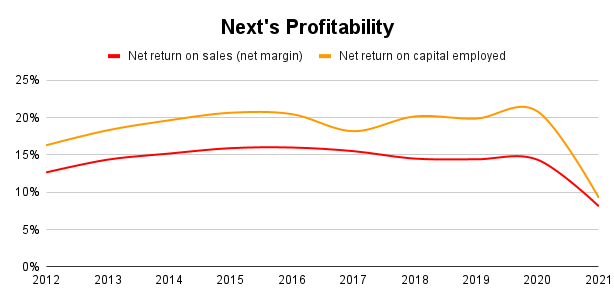

Next has produced consistently high returns and growth

Most high-quality companies generate above-average returns on capital employed (factories, warehouses, stores, inventory, etc) and Next is no different. If we ignore the pandemic, Next’s net return on capital (net ROCE) has averaged almost 20% over the last decade, including the value of its not-inconsiderable store estate.

20% is about double the UK average return on capital of 10%, so Next must have some sort of durable competitive advantage. If it didn't, those high profits would have been competed away by now.

The good thing about high profits is that they give companies cash to reinvest for growth, and that’s exactly what Next has done. Over the years, the capital employed in the business (stores, equipment etc) has increased, and that has driven higher revenues and earnings.

In addition, Next has consistently used some of that cash to buy back its own shares, driving even faster per share dividend growth, which is exactly what dividend growth investors are looking for.

Next has several durable competitive advantages

Very few clothing retailers have durable competitive advantages because it’s easy to design a t-shirt, have a few hundred manufactured in China and either rent a store or sell them on Amazon. Obviously, it’s a bit more complicated than that, but the reality is that retail is a brutally competitive business and most retailers are not highly profitable.

When a retailer is highly profitable over at least several decades, it’s usually down to one of three things:

-

Brand - The business owns a loved brand which allows it to charge higher prices without losing sales

-

Scale - The business is the market leader which gives it almost unbeatable economies of scale

-

Expertise - The business is exceptionally well-run and is a master at its trade.

Brand - While Next has a very well-known brand and while it may be loved by some, I don’t see the Next brand as being a key differentiator.

Being so well-known obviously helps, as does having most people know where your products sit in the quality/price spectrum, but here’s a thought experiment:

If you could buy a coat that was equal in quality to a coat from Next but was half the price, would you buy the coat from Next or the cheaper alternative? Everyone I asked said they’d buy the half-price coat because owning a coat from Next wasn’t a big deal.

Running the same experiment using Burberry and I got the opposite answer. Everyone I asked said they’d buy a Burberry coat for £2,000 rather than a non-Burberry but otherwise identical coat because clearly, price isn’t a major factor if you’re paying that sort of money for a coat.

In other words, the Burberry brand has a lot of pricing power. Next doesn’t.

Here's my recent post-sale review of Burberry: Is Burberry a good dividend growth stock?

Scale - Next is a very large clothing and homewares retailer and as far as I can tell, it's the largest in the UK in terms of profit.

Scale is an important competitive advantage because it can provide all sorts of advantages. For example:

- You buy more stock so you have more bargaining power with suppliers

- Your warehouses and sorting depots are bigger and bigger tends to mean more efficient

- You make more profit so you can offer talented people more money to work for you

- You can offer talented people a more diverse career within a higher-profile organisation.

So scale can be an excellent advantage, and Next certainly has scale.

Expertise: Expertise is built by deliberately practising a narrow set of skills over a long period of time. In business, this means operating the same narrowly focused core business for decades. In Next’s case, it started life in 1870 as Kendall & Sons, a high-quality umbrella, rainwear and ladieswear manufacturer and retailer. In 1981, Kendall & Sons was purchased by a larger menswear retailer, Hepworth & Sons, and the name was changed to Next.

So Next has been a clothing retailer since the 19th century, which is more than enough time to build up some expertise.

Of course, operational expertise has to be combined with expertise at the board level, because an idiotic CEO can easily undo all the operational expertise in the world.

Fortunately for Next, it seems to have lucked into having a very unusual CEO by the name of Simon Wolfson.

Wolfson is unusual because he joined Next almost straight out of university, in 1991, as the son of the company’s Chairman. He seems to have been given a magic carpet ride to the top, becoming retail sales director in 1993, managing director in 1999 and CEO in 2001. At 33 years old, he was the FTSE 100’s youngest CEO.

That looks a lot like nepotism, but fortunately for Next, things have actually worked out very well.

Wolfson is nothing like a typical career CEO. He has been the CEO of Next for more than 20 years and seems to have no interest in going anywhere else. Ever.

So unlike many CEOs who try to make a big impact in a few years so they can jump ship to a bigger and better (paid) opportunity elsewhere, Wolfson runs Next like a family business. In other words, he runs it as if the company was going to be his children's and grandchildren's only source of income for the next 100 years.

Rather than setting eye-catching goals such as doubling revenues or profits in the next five years, his approach is to continually evolve Next so that it is both highly profitable today while being well-positioned for the next decade and beyond. Wolfson calls this “following the money” while others call it “moving the ship into fast-flowing water”.

This focus on long-term success is why Next has had an online business for more than 20 years and generates more sales online than in-store. It’s also why the company has little debt, only signs short leases on its stores (to increase flexibility) and has spent the last few years building out its Total Platform business.

In short, Next appears to combine both deep operational expertise with extremely sensible management whose interests seem to be aligned to those of long-term shareholders. And that is a rare combination and a durable competitive advantage.

The only issue with having management as a competitive advantage is the question of who takes over if Wolfson gets hit by the proverbial bus? My preference is for companies to build a pipeline of internal CEO candidates as that (a) shows a commitment to developing its employees and (b) it helps to retain the best talent as they can see a clear path to the top.

Wolfson was an internal hire, but also under very unusual circumstances, so there's no way of knowing what will happen when he leaves the company (for whatever reason).

Estimating Next's future dividends

So Next is, in my opinion, a high-quality dividend stock that I would be happy to own (and already do).

The next step in my five-step strategy for investing in dividend stocks is to come up with a fair value estimate for the company, and that begins with building a model of the company's future dividends.

Next’s ordinary dividend peaked at 165p in 2019 and was then suspended during the pandemic. If we include special dividends and cash paid out as share buybacks, Next's peak cash return to shareholders actually peaked in 2016 at almost 550p per share.

The company paid a 110p special dividend in the first half of this year and is likely to pay a total special dividend of anywhere between 200p and 300p for the full year.

Management has said that earnings per share are likely to be around 517p, so my dividend model will start there. I'm going to assume a dividend cover of two in FY 2022 (this year), which equates to a full-year dividend of 258p, which is consistent with the 110p half-year special dividend.

More important than next year's dividend is dividend growth beyond that, so let's think about that.

In my opinion, dividend models should be based on a mixture of internal and external growth factors:

-

Internal growth factors: The main internal factors are the returns the company earns on its capital and how much of those returns it can reinvest into additional assets to drive growth.

-

External growth factors: The main external factors are the size of the existing market, the ability of the company to grow within that market and its ability to expand into adjacent markets.

Next is a dominant player in a very mature market, so growth is likely to be constrained by external factors rather than internal factors.

My baseline assumption then is that Next is unlikely to grow much faster than the overall UK economy, which has an expected growth rate of around 3%.

With that top-level assumption in place, I can then build a simple model which has Next growing by around 3% per year "forever", and we'll see what that means for future dividends.

As I've already mentioned, Next has historically returned cash to shareholders mostly through large share buybacks and special dividends, with a relatively small ordinary dividend. The combined payout peaked in 2016 at 480p per share, so that gives us a baseline to think about future dividends.

And for the sake of simplicity I will assume that in future, Next pays cash out as a single large ordinary dividend rather than a mix of ordinary dividends, special dividends and buybacks.

Here are the main facts and assumptions which underpin my dividend model:

-

Next had capital employed (warehouses, stores, inventory, etc) valued at 2,400p per share in 2021.

-

Next will earn 516p in 2022, as per management guidance (this requires a net return on capital of 21.5% which is within Next’s normal range)

-

The 2022 total dividend is 192p, in line with management's guidance, giving a dividend cover of 2.7 which is abnormally high. The undistributed earnings are reinvested within the business to drive growth.

-

In 2023 and beyond, the net return on capital declines to 18% which is close to Next’s historical average.

-

A net return on capital of 18% in 2023 generates earnings of 491p. Dividend cover returns to the historically normal level of 1.2 and that produces a dividend of 409p. That sounds high, but it's well below Next's peak 2016 dividend (plus specials and buybacks).

-

The cash which is reinvested within the business drives a growth rate of around 3% per year to 2030.

-

Beyond 2030 I assume long-term dividend growth at the same 3% per year. That's in line with the expected growth rate of the UK economy and is conservative given that Next also has a growing international business.

I think those assumptions are realistic and conservative, both of which are essential features of a sensible dividend model.

Plugging those assumptions into my Dividend Stocks Spreadsheet produces the following table:

The model shows earnings reaching 604p in 2030 compared to a pre-pandemic high of 470p in 2020. That's a nearly 30% increase, but it's over ten years so I think it's realistic.

The model also estimates that dividends will reach 503p in 2030, which is a yield of 6.3% on the current share price of £79.80. That sounds pretty good to me and I don't think it's unreasonable given that Next paid out almost that much in 2016.

Estimating fair value, good value and the margin of safety

Fair Value in the table above is the price at which Next would provide a market-average return. In other words, if the model turns out to be correct (which of course it won’t be as it’s only an estimate) then buying Next at the fair value price of £108.63 and holding the shares forever would give you an annualised return of 7%.

Good Value is the same idea, but the return from buying Next at the good value price of £60.43 and holding it forever would be 10% annualised.

In principle, my goal is to buy quality dividend stocks when they’re cheaper than good value and sell when they’re above fair value. For a variety of reasons it doesn't always work out quite like that in practice, but that's the goal.

The Margin of Safety in the table above comes from step three of my five-step investment strategy, which is to buy stocks when there's a significant margin of safety.

The Margin of Safety score basically tells you where the current price is in relation to the good and fair value prices.

When the current price equals fair value, the margin of safety is zero and when the current price equals the good value price, the margin of safety is 100%.

Next’s share price is currently £79.80, so it’s around halfway between the model's fair value estimate of £96.41 and the good value estimate of £54.95. That’s why its margin of safety is 40%.

With a margin of safety of 40%, Next is roughly halfway between where I'd like to buy and where I'd probably sell. Ideally, I'm looking for a margin of safety of more than 100%, and at the very least 50%. So although I'm happy for Next to remain in the UK Dividend Stocks Portfolio, I probably wouldn't buy at this price because it's too close to my fair value estimate.

At the very minimum, I'd like the share price to be below £70 before buying, but I'd be much happier if the shares fell below £60. At that price, I would almost definitely be looking to buy.

No time for spreadsheets or annual reports?

If you like this article but don’t have hours each month to dig through company accounts, you might find my monthly investment newsletter useful.

Once a month I send out a plain‑English PDF showing:

- The full UK dividend stocks model portfolio

- Which shares I’m buying, selling, trimming or topping up

- The latest news and trading updates for each holding

- Where we are in the stock market valuation cycle

All designed so a UK investor can stay on top of their dividend portfolio in well under an hour a month.

Get the latest blog posts & a free checklist

Get my latest articles in (at most) one email per week and download my dividend investing checklist. Topics usually include:

- Detailed reviews of high-quality UK dividend stocks

- Updates on my UK dividend stocks portfolio

- FTSE 100 and FTSE 250 valuations

- "How to" articles covering all aspects of dividend investing

No spam. Unsubscribe anytime.